First-Time Homebuyer Programs in 2026: Grants, Loans, and Expert Tips

Share:

Table of Contents

- 1. The 2026 housing market: Why first-time homebuyer programs matter

- 2. Deep dive: FHA loans 2026

- 3. Maximizing down payment assistance in 2026

- 4. Unlocking first-time buyer grants: The "free money" reality

- 5. At-a-glance comparison (FHA vs. DPA vs. Grants)

- 6. Your step-by-step action plan to take advantage of first-time homebuyer programs in 2026

- 7. Pro tip: Looking past the listing photos

- 8. Frequently asked questions (FAQs) about first-time homebuyer programs in 2026

- 9. Conclusion

Stepping into the housing market can feel like navigating a storm. While interest rates are finally stabilizing, stubborn home prices still make homeownership feel out of reach for many. If you are struggling to save a massive 20% down payment, you are not alone, and more importantly, you are not out of options. The landscape has shifted, and a variety of first-time homebuyer programs in 2026 are stepping up to bridge the gap. From low-interest government loans to forgivable cash grants, this article will break down the best financial tools available today to help you confidently unlock your first front door.

Also read:

- Best Real Estate Coaching Programs in 2026: Costs & How to Choose

- How California Agents Use Virtual Staging to Win Listings: A Case Study

1. The 2026 housing market: Why first-time homebuyer programs matter

The 2026 real estate landscape presents a unique set of challenges for anyone trying to transition from renting to owning. While the frantic bidding wars of the past few years have finally cooled down, buyers today face a stark reality: home prices remain stubbornly high, and mortgage interest rates, though stabilizing, demand a much larger monthly commitment than they did a decade ago. For everyday people, the traditional advice of "just save up 20%" feels completely out of touch with reality.

First-time homebuyer programs are of immense assistance for hesitant buyers in 2026 to overcome financial and psychological barriers.

First-time homebuyer programs are of immense assistance for hesitant buyers in 2026 to overcome financial and psychological barriers.

Today’s first-time buyers face a dual financial hurdle. The first is immediate liquidity, the massive mountain of upfront cash required for a down payment and closing costs. When high rent and everyday inflation consume a large portion of your paycheck, accumulating tens of thousands of dollars is an exhausting, slow-motion process. The second hurdle is monthly affordability, as higher rates compress your purchasing power.

This is precisely why utilizing specialized buyer assistance is no longer just a luxury; it is a critical strategic move. Recognizing these steep economic barriers, federal, state, and local governments have heavily revised their budget allocations for 2026 to inject fresh funding into housing finance agencies. These programs are specifically engineered to level the playing field, allowing you to preserve your hard-earned emergency savings while still securing a home. In 2026, the real key to becoming a homeowner isn’t just working harder to save every penny; it’s about buying smarter by leveraging the public funds explicitly earmarked to help you succeed.

2. Deep dive: FHA loans 2026

When it comes to breaking into homeownership without a massive financial safety net, Federal Housing Administration (FHA) loans remain the gold standard. Insured by the government, these loans minimize the risk for private lenders, allowing them to offer highly competitive terms to everyday buyers. If you are struggling with a flawless credit history or a massive savings account, FHA loans 2026 are designed precisely to keep the dream of owning a home within your reach.

2.1. New FHA loan limits for 2026

To keep pace with the shifting real estate market, the Department of Housing and Urban Development (HUD) has adjusted its maximum lending thresholds. In 2026, the baseline FHA loan limit, often referred to as the "floor" for low-cost counties, has been set at $541,287 for a single-family home. Conversely, if you are house hunting in a competitive, high-cost metropolitan market like Los Angeles or New York City, the maximum lending "ceiling" scales up significantly to $1,249,125. To find the exact configurations for your specific location, you can check HUD's official FHA Mortgage Limits lookup tool, which reflects all real-time adjustments for the current year. These updated limits mean you have more room to negotiate and buy a competitive starter home, even in pricier suburbs.

The limit of the FHA loan, one of the most prominent first-time homebuyer programs in 2026, varies by region.

The limit of the FHA loan, one of the most prominent first-time homebuyer programs in 2026, varies by region.

2.2. Credit score and down payment requirements

The biggest draw of FHA loans 2026 is their highly forgiving credit criteria. Unlike conventional loans that penalize you heavily for past financial hiccups, the FHA framework uses a tiered system that heavily favors motivated buyers:

- FICO® score of 580 or higher: You qualify for the absolute minimum down payment of just 3.5%. For a $400,000 home, that means you only need $14,000 upfront.

- FICO® score between 500 and 579: You can still get approved, but you will be required to put down a 10% down payment to offset the lender's risk.

Additionally, the FHA allows 100% of your down payment to come from a verified family gift, making it much easier to cross the finish line if you have relatives willing to help.

2.3. Understanding mortgage insurance premiums (MIP)

Because FHA loans require a lower barrier to entry, the government protects lenders through Mortgage Insurance Premiums (MIP). As a borrower, you will navigate two types of MIP: an upfront premium (usually 1.75% of the loan amount, which can be rolled directly into your total balance) and an annual premium that is divided and paid monthly. While MIP adds a small buffer to your monthly payment, it is the small price paid to unlock a mortgage that traditional banking rules would otherwise deny you.

3. Maximizing down payment assistance in 2026

For most aspiring homeowners, the ultimate hurdle isn’t qualifying for a monthly mortgage payment; it’s surviving the initial cash grab at the closing table. Accumulating an extra $15,000 to $30,000 for a down payment while simultaneously paying record-high market rents can feel nearly impossible. This is where maximizing down payment assistance 2026 programs becomes a total game-changer. These initiatives act as a financial bridge, stepping in to supply the upfront capital required so you can buy a home without completely draining your life savings.

3.1. How DPA programs work

Down Payment Assistance (DPA) programs are rarely structured like standard bank loans. Instead, these types of first-time homebuyer programs in 2026 typically operate under two primary, buyer-friendly financial vehicles:

- Forgivable second mortgages: With this setup, a state or local agency provides the down payment funds as a secondary loan that requires zero monthly payments. If you remain in the property as your primary residence for a specified period (typically 5 to 10 years), the entire debt is wiped clean.

- Deferred-payment loans: While this type of loan does eventually need to be repaid, it features 0% interest and requires no active monthly payments. The balance only becomes due when you sell the home, refinance your mortgage, or finally pay off your primary loan.

3.2. Finding funds through state housing finance agencies (HFAs)

The bulk of the down payment assistance 2026 funds are not administered directly by the federal government. Instead, they flow through state-level Housing Finance Agencies (HFAs), such as CalHFA in California or the Texas State Affordable Housing Corporation (TSAHC). Because these funds are localized, the perks vary by region. Some states offer a flat grant of $10,000, while others provide a percentage match, covering up to 3% to 5% of your total purchase price. The smartest way to start your search is by consulting the National Council of State Housing Agencies (NCSHA) directory to identify the legitimate government-backed finance programs operating in your specific state. The trick is working with an HFA-certified lender, as many traditional big-box banks do not participate in these localized state programs.

There’s plenty of financial assistance for first-time homebuyers out there.

There’s plenty of financial assistance for first-time homebuyers out there.

3.3. Targeted assistance and first-generation buyers

In 2026, many DPA programs have added hyper-targeted categories to fast-track specific buyers. "Good Neighbor" programs offer substantial financial bonuses for educators, law enforcement, first responders, and healthcare professionals. Furthermore, 2026 has seen an unprecedented expansion of first-generation homebuyer assistance. If your parents do not currently own a home, you may qualify for enhanced funding tiers, sometimes unlocking up to $25,000 in pure down payment and closing cost support.

4. Unlocking first-time buyer grants: The "free money" reality

The phrase "free money" naturally triggers skepticism, but when it comes to the real estate market, first-time buyer grants are a legitimate reality. Unlike standard loans or even deferred-payment secondary mortgages, a true grant is a financial award that does not have to be repaid. In a challenging market, securing a grant can mean the difference between buying a home now or delaying your plans for several more years. However, these funds do not just fall into your lap; they come with strict guardrails and a specific set of rules.

4.1. Navigating the sources of grant funding

Grants originate from a mix of federal, state, and local municipality budgets. At the federal level, the Department of Housing and Urban Development (HUD) distributes block grants to local communities, which then package them for individual buyers. On a more localized level, many city and county governments run specialized programs funded by local tax initiatives. These are specifically designed to keep young professionals and working-class families from being priced out of their own neighborhoods.

You can seek grant funding from multiple sources, such as federal, state, and local municipalities.

You can seek grant funding from multiple sources, such as federal, state, and local municipalities.

4.2. The gatekeepers: Strict eligibility standards

Because these funds are heavily subsidized, the application process is rigorous. To qualify for most first-time buyer grants, you must meet precise criteria:

- Income caps: Your household income is typically capped at a specific percentage, usually 80% to 120%, of your region’s Area Median Income (AMI). Buyers can cross-reference their financial standing directly through HUD’s income limits datasets to see if they qualify for localized community grants.

- Purchase price limits: The home you are buying must fall under a certain appraisal value to ensure the funds are going toward actual starter homes rather than luxury properties.

- Homebuyer education: You will almost always be required to complete a HUD-approved homebuyer education course. These quick classes teach you the fundamentals of budgeting, maintaining a home, and managing a mortgage.

4.3. The "catch": Understanding residency requirements

While you do not have to pay the money back, it is not entirely unconditional. Most grants feature a "recapture period", a legal clause requiring you to use the property as your primary residence for a set number of years, usually between three and five. If you decide to sell the home, rent it out, or refinance your mortgage before that clock runs out, you will have to pay back a prorated portion of the grant. But if you settle down and stay put, the money becomes yours entirely, serving as an incredible equity boost from day one.

5. At-a-glance comparison (FHA vs. DPA vs. Grants)

Finding what’s applicable among first-time homebuyer programs in 2026 can quickly become overwhelming. To help you choose the best financial path for your specific situation, here is a quick, direct comparison of how these three primary options stack up in the 2026 market.

|

Program type |

Primary purpose |

Repayment required? |

Ideal candidate |

|

FHA Loans 2026 |

Lowers the barrier to mortgage approval with lenient credit rules. |

Yes, via standard monthly mortgage payments and MIP. |

Buyers with lower credit scores (580+) or limited personal savings. |

|

Down Payment Assistance 2026 |

Covers the heavy upfront cash needed for your down payment. |

Varies; often structured as 0% interest or forgivable loans. |

Buyers who can afford monthly payments but lack immediate cash. |

|

First-Time Buyer Grants |

Provides true "free money" for initial closing and down payment costs. |

No, provided you meet the required primary residency timeline. |

Low-to-moderate-income buyers who meet regional caps. |

Remember, you do not have to choose just one. Many savvy buyers stack a localized grant on top of an FHA loan to minimize their out-of-pocket costs to almost zero.

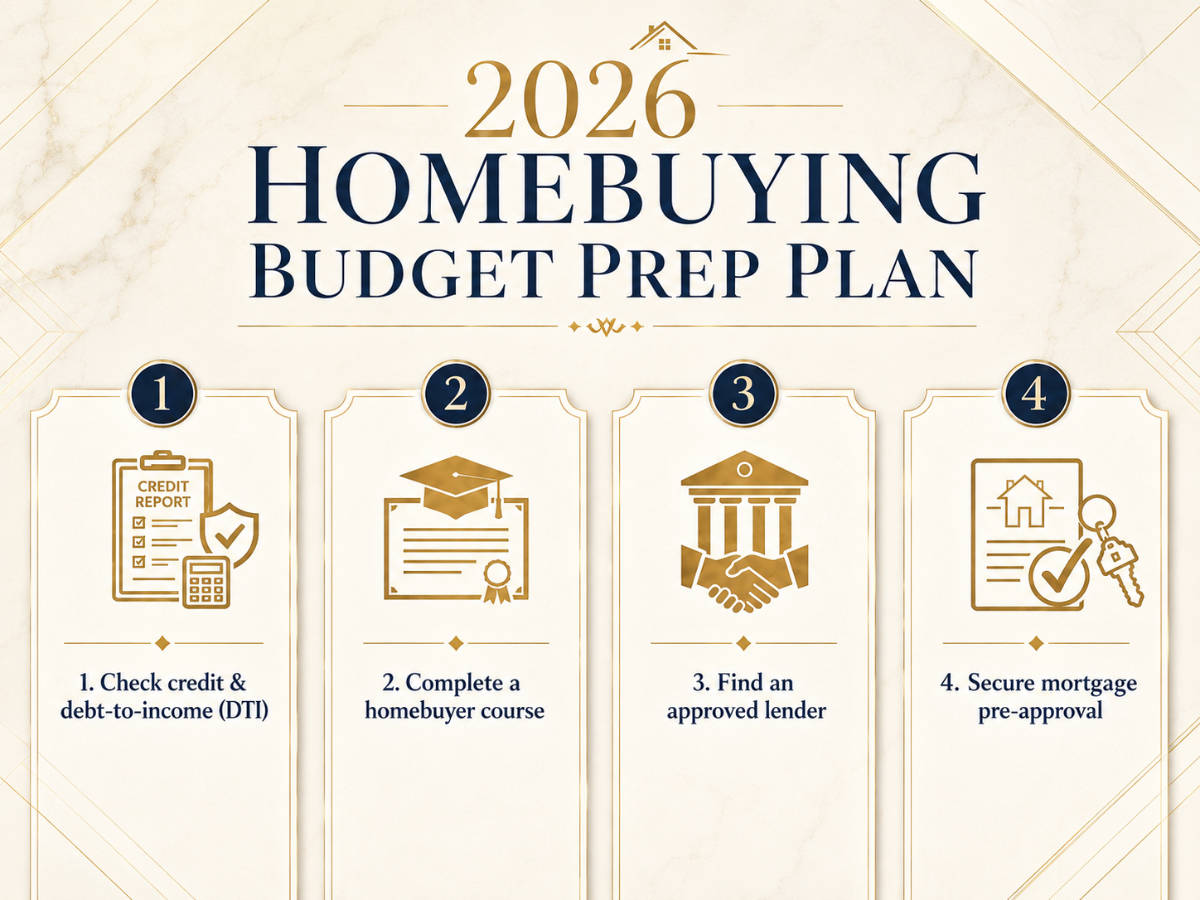

6. Your step-by-step action plan to take advantage of first-time homebuyer programs in 2026

Transforming all these financial options into a physical set of keys requires an organized, strategic approach. To claim your funding without unnecessary stress, use this sequential step-by-step action plan designed for the 2026 mortgage market.

A detailed plan prepares you better for budgeting for your first home.

A detailed plan prepares you better for budgeting for your first home.

1. Check credit & debt-to-income (DTI): Month 1.

Pull your free credit reports from the major bureaus, dispute any reporting errors, and calculate your current DTI ratio. Avoid opening new credit lines or changing jobs during this critical preparation window.

2. Complete a homebuyer course: Month 2.

Most state housing finance agencies and grant programs mandate a HUD-approved homebuyer education certificate before they will release any funds. You can easily locate a verified, budget-friendly program through a HUD-approved housing counseling agency to complete this quick requirement early and avoid unexpected closing delays.

3. Find an approved lender: Months 2-3.

Not all big-box banks participate in local grants or specialized down payment programs. You must interview and select an experienced, certified lender who specifically specializes in pairing FHA loans with localized assistance.

4. Secure mortgage pre-approval: Month 3.

Submit your official financial documentation (tax returns, W-2s, bank statements) to secure a formal mortgage pre-approval letter. This locks in your active house-hunting budget and proves to sellers you are ready.

By checking these boxes in order, you protect your credit score and ensure you are fully qualified the moment you find your dream home.

7. Pro tip: Looking past the listing photos

Once you secure your pre-approval, the real house hunting begins on platforms like Zillow or Realtor.com. Here is an insider secret: many affordable starter homes suffer from terrible marketing. It is incredibly common to encounter dark, cluttered, or entirely empty listing photos that completely fail to showcase a property’s true potential. Don't let bad photography scare you away from a home with "good bones."

Virtual staging can reveal the potential of many affordable vacant properties.

Virtual staging can reveal the potential of many affordable vacant properties.

On the flip side, pay close attention to listings that leverage professional image editing and virtual staging. Forward-thinking real estate professionals often collaborate with expert platforms like Fotober to digitally enhance lighting, remove clutter, and transform vacant spaces into beautifully rendered, fully furnished rooms. Use these virtually staged images as your ultimate design blueprint. They allow you to see exactly how an empty space can look, helping you spot hidden market value that other buyers completely miss.

8. Frequently asked questions (FAQs) about first-time homebuyer programs in 2026

Q: Can I combine a first-time buyer grant with an FHA loan?

A: Absolutely. Combining or "stacking" programs is a highly effective strategy in the 2026 market. Many buyers use an FHA loan for its lenient credit guidelines and layer a localized grant on top to cover the required 3.5% down payment and closing costs, reducing out-of-pocket expenses to nearly zero.

Q: Am I considered a first-time buyer if I have owned a home in the past?

A: Yes, quite likely. According to HUD guidelines, you legally qualify as a first-time homebuyer if you have not owned a primary residence at any point during the three years leading up to your new home purchase.

Q: Do all 2026 assistance programs have strict income limits?

A: Most do. Because these grants and down payment programs are publicly funded, they are reserved for low-to-moderate-income households. Income caps are typically tied to your region, usually limiting applicants to between 80% and 120% of the Area Median Income (AMI).

9. Conclusion

Navigating the 2026 housing market may seem daunting, but you do not have to do it alone. By leveraging first-time homebuyer programs in 2026: FHA loans, maximizing down payment assistance, and unlocking first-time buyer grants, the path to homeownership becomes highly achievable. You no longer need a massive personal fortune to buy your first home; you just need a smart, strategic plan.

Because many of these state and local grant programs operate on a first-come, first-served basis with capped annual budgets, time is of the essence. Take the next step today by contacting a HUD-approved housing counselor or an HFA-certified lender to secure your funding.

Connect with Fotober

- Facebook: fotobermedia.co

- YouTube Channel: Fotober

- TikTok Channel: @fotober

- Instagram: fotober_media

- Email support: [email protected]

- Hotline: +84 942 110 297.

Related posts

How to Choose a 3D Architectural Rendering Company for Real Estate

August 5, 2026

Why You Must Have 3D Exterior Rendering For Your Project in 2026

August 5, 2026

3D Interior Rendering to Shape Your Dream Home in 2026

August 4, 2026

Finest 3D Architectural Rendering Software to Bring Blueprints to Life

August 3, 2026