Real Estate 2026 predictions: Opportunities, Challenges, and Key Trends

Share:

Table of Contents

- 1. Overview of the Real Estate Market 2025

- • 1.1. Inventory Expansion Without Full Relief

- • 1.2. High Interest Rates Remain a Structural Constraint

- • 1.3. Price Growth Loses Steam

- • 1.4. Affordability Still the Central Challenge

- • 1.5. New Construction Gains Strategic Importance

- • 1.6. Shift Toward a More Balanced Market

- • 1.7. Demographic Demand Continues to Evolve

- 2. Macroeconomic Policies and Their Impact on Real Estate Heading into 2026

- 3. Key Factors Shaping the Real Estate Market in 2026

- 4. Real Estate 2026 Predictions by Market Segment

- 5. Real Estate 2026 Predictions: Rental Market Outlook

- 6. Visual Marketing Becomes a Competitive Differentiator

- 7. Conclusion: What Real Estate 2026 Means for the Industry

As the U.S. real estate market approaches 2026, the conversation is no longer about recovery - it is about recalibration. After years of unprecedented volatility driven by pandemic-era stimulus, rapid interest rate hikes, and shifting buyer behavior, the industry is entering a more complex and selective phase. Supply conditions are loosening, affordability remains constrained, and demand is fragmenting across regions, demographics, and property types. So, what are real estate 2026 predictions and trends?

Understanding predictions for 2026 real estate therefore requires looking beyond surface-level indicators such as price movements or transaction counts. Instead, it demands a deeper examination of structural forces - macroeconomic policy, demographic transitions, financing conditions, and technological adoption-that are quietly reshaping how homes are built, marketed, and transacted. This analysis explores the key trends, risks, and opportunities likely to define the U.S. real estate market in 2026, offering a strategic lens for investors, developers, and industry professionals navigating the next stage of the property cycle.

1. Overview of the Real Estate Market 2025

What changes has the real estate market experienced in 2025? Before delving into real estate 2026 predictions let’s review the market in 2025.

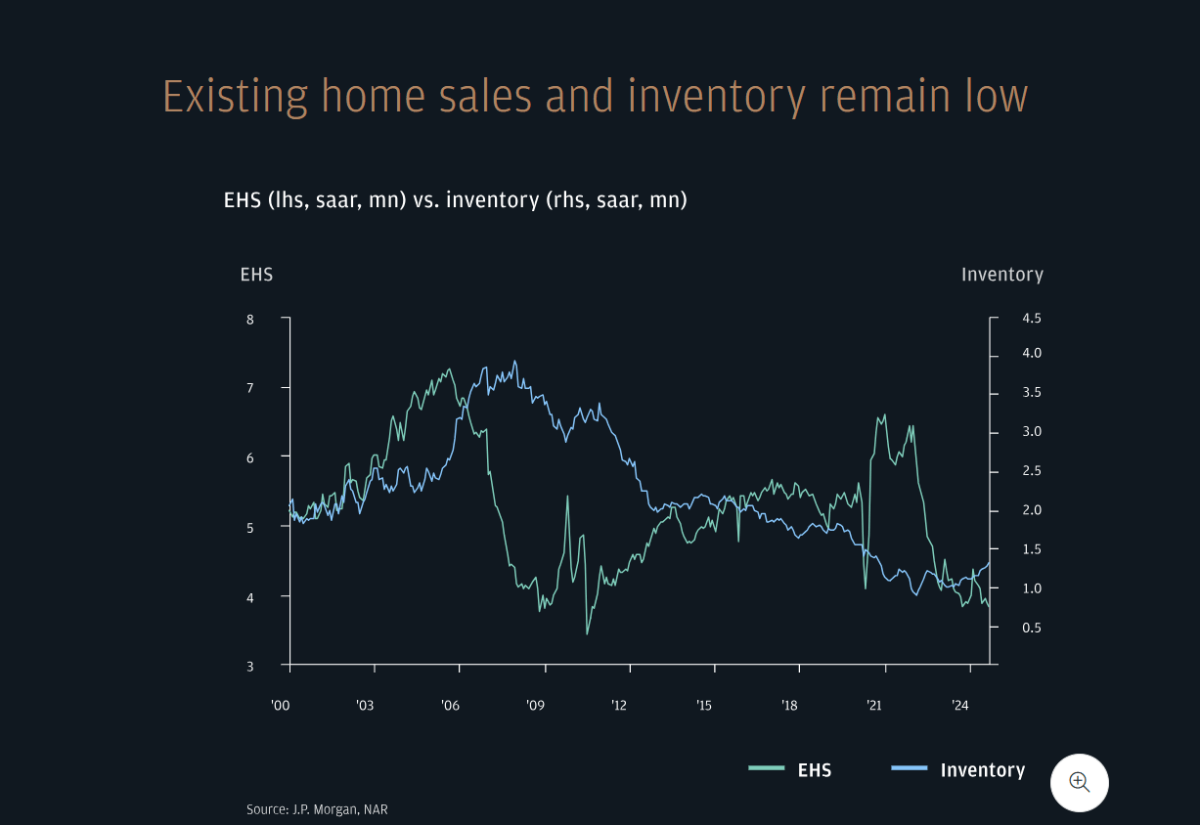

As the U.S. housing market moved through 2025, it entered a phase of recalibration rather than recovery. Supply conditions began to loosen - largely driven by new residential construction-yet affordability remained under pressure as borrowing costs stayed elevated. Mortgage rates hovering near the 6.7–6.9% range continued to limit purchasing power, reshaping buyer behavior and slowing transaction velocity. The result was a market trending toward equilibrium, where competition softened but demand did not disappear, especially for smaller, cost-efficient properties.

Chart: Existing home sales and inventory remain low. Source: J.P Morgan.

1.1. Inventory Expansion Without Full Relief

Housing availability climbed to its highest levels since the post-pandemic rebound, with total listings rising sharply year over year. However, the pace of newly added homes did not fully match this growth, suggesting that much of the increase came from properties staying on the market longer rather than a surge of fresh supply.

1.2. High Interest Rates Remain a Structural Constraint

Despite expectations of gradual rate adjustments, mortgage costs remained stubbornly high throughout 2025. Elevated monthly payments continued to sideline many first-time buyers, reinforcing cautious purchasing decisions and limiting price momentum.

1.3. Price Growth Loses Steam

Home values showed signs of stagnation across many regions. Builder incentives, rate buy-downs, and competitive pricing in new developments reduced upward pressure on prices, offering buyers alternatives to resale homes.

1.4. Affordability Still the Central Challenge

Even with improved selection, affordability did not materially improve for large segments of the population. High financing costs meant that median-income households in several metros remained priced out, with affordability gaps varying widely by region.

1.5. New Construction Gains Strategic Importance

Developers increased activity and leaned heavily on incentives, positioning newly built homes as a compelling option compared to existing inventory. In some markets, new construction became the primary driver of transaction volume.

1.6. Shift Toward a More Balanced Market

Many areas experienced a clear transition away from seller-dominated conditions. Average time on market extended to nearly two months in mid-2025, signaling reduced urgency among buyers and greater negotiation flexibility.

1.7. Demographic Demand Continues to Evolve

Younger buyers - particularly Millennials and Gen Z-continued to shape demand patterns, prioritizing smaller footprints, smart-home features, and neighborhoods compatible with remote or hybrid work lifestyles.

2025 stands out as a turning point rather than a downturn. Supply-side improvements helped stabilize the market, but persistent financing costs prevented a full reset. Moving into 2026, the U.S. housing market is likely to remain selective and segmented - rewarding realistic pricing, efficient home designs, and strategies aligned with changing buyer priorities.

2. Macroeconomic Policies and Their Impact on Real Estate Heading into 2026

Looking toward real estate 2026 predictions, macroeconomic policy remains one of the most decisive forces shaping the U.S. property market. Throughout 2025, real estate operated under sustained financial pressure as monetary tightening, cautious banking behavior, and shifting regulatory frameworks collectively reshaped investment conditions. Elevated inflation and uneven economic momentum added further complexity, forcing market participants to reassess risk, pricing, and long-term strategy.

Chart: The impact of different factors on the market.

2.1. Monetary Policy and Interest Rate Dynamics

The Federal Reserve’s policy stance continued to set the tone for real estate financing. While potential rate adjustments could offer incremental relief to mortgage borrowers, borrowing costs remained materially higher than pre-pandemic norms. This environment limited refinancing opportunities and placed additional stress on income-producing properties, particularly those with floating-rate debt structures. At the same time, inflation-though moderating-kept development, labor, and maintenance expenses elevated, increasing the total cost of property ownership across both residential and commercial segments.

2.2. Bank Lending Conditions and Credit Availability

Real estate 2026 predictions: Credit markets grew increasingly selective in 2025. Banks, facing tighter regulatory oversight and balance sheet constraints, reduced exposure to higher-risk real estate assets. Commercial property owners encountered greater difficulty securing new financing or extending existing loans, especially within office and underperforming sectors. As a large volume of commercial real estate debt approaches maturity, refinancing at higher interest rates has become a central risk, forcing some owners to contribute additional equity or consider asset repositioning.

2.3. Fiscal, Trade, and Regulatory Influences

Policy decisions beyond monetary tightening also played a critical role in shaping real estate outcomes. Adjustments to tax provisions-such as depreciation rules-redirected investment toward specific asset classes with stronger long-term demand. Meanwhile, higher trade tariffs increased construction input costs, compressing development margins and slowing project pipelines. Environmental regulations, alongside rising insurance premiums linked to climate-related risks, further altered underwriting assumptions, particularly in disaster-prone regions. Political cycles added another layer of uncertainty, as shifts in leadership can influence taxation, housing policy, and labor availability.

2.4. Uneven Impact Across Real Estate Sectors

The effects of these macro forces varied widely by property type. In residential markets, sustained borrowing and ownership costs reinforced rental demand, while many buyers recalibrated expectations around long-term mortgage rates. Within commercial real estate, performance diverged sharply: assets tied to digital infrastructure, logistics, and select multifamily or retail segments showed relative resilience, whereas office properties faced mounting pressure due to declining demand and refinancing hurdles.

2.6. Macro Takeaway for Real Estate 2026 Predictions

From a real estate 2026 predictions standpoint, macroeconomic policy is unlikely to provide a rapid tailwind for the property market. Instead, 2026 is shaping up to be a year where disciplined capital allocation, asset quality, and adaptive financing strategies matter more than broad market cycles. Investors and operators who account for persistent policy-driven constraints will be better positioned to navigate the next phase of the real estate cycle.

3. Key Factors Shaping the Real Estate Market in 2026

Understanding real estate 2026 predictions requires looking beyond short-term price movements and focusing on structural forces that influence demand, supply, and investor behavior. Among these, demographics, interest rates, economic conditions, and government policy remain the most decisive drivers.

Key factors shaping the real estate market by 2026 predictions.

3.1. Demographic Shifts

Demographics describe the composition and movement of a population, including age distribution, income levels, household size, migration patterns, and population growth. While often overlooked, demographic trends tend to exert long-lasting influence on real estate markets-sometimes over multiple decades-by shaping housing preferences and location demand.

One of the most impactful demographic forces continues to be the aging of the baby boomer generation, born between 1945 and 1964. As this cohort entered retirement beginning in the early 2010s, its influence on housing demand became increasingly visible and is expected to persist well into the coming decade.

These demographic transitions raise critical questions for investors and developers heading into 2026, such as:

-

How will retirement-driven migration affect demand for second homes in established resort and leisure destinations?

-

In what ways will lower household incomes and smaller family sizes-resulting from children leaving home-reduce demand for large, single-family residences?

By anticipating these shifts early, market participants can narrow their focus toward property types and locations that align with emerging demographic realities before broader trends fully materialize.

3.2. Interest Rates and Financing Costs

Interest rates remain one of the most influential variables in real estate 2026 predictions. Changes in borrowing costs directly affect affordability, purchasing power, and overall transaction volume. Lower interest rates reduce mortgage payments, making homeownership more accessible and often stimulating demand-sometimes at the expense of higher prices. Conversely, rising rates increase financing costs, cooling demand and placing downward pressure on valuations.

The impact of interest rates extends beyond residential housing. For income-producing assets such as real estate investment trusts (REITs), the relationship between rates and pricing closely resembles that of bonds. When interest rates decline, fixed-income alternatives become less attractive, increasing the appeal of higher-yielding REITs and supporting their valuations. As rates rise, REIT yields become relatively less competitive, often leading to price adjustments.

Understanding this dynamic is essential for evaluating both direct property investments and real estate securities in a higher-for-longer rate environment.

3.3. Overall Economic Conditions

The broader health of the economy plays a central role in determining real estate performance. Indicators such as GDP growth, employment trends, manufacturing activity, and commodity prices offer insight into the economy’s capacity to support housing demand and commercial occupancy. In general, periods of economic slowdown tend to weaken real estate markets, though the impact varies significantly by asset class.

Real estate’s sensitivity to economic cycles differs across sectors. For example, properties tied to hospitality typically experience sharper downturns during recessions due to the short-term nature of hotel stays, which can be canceled quickly when consumer confidence declines. In contrast, office and industrial properties often benefit from longer lease structures that provide income stability even during economic contractions.

Recognizing where each asset type sits within the economic cycle is critical for managing risk and aligning investment strategy with macroeconomic conditions.

3.4. Government Policy and Regulation

Public policy remains a powerful force influencing real estate demand and pricing. Governments can temporarily stimulate activity through tax credits, deductions, subsidies, or regulatory changes, often altering supply-demand dynamics in ways that may not be immediately apparent.

A notable example occurred during the late 2000s, when the U.S. government introduced a tax credit for first-time homebuyers to support housing demand amid economic weakness. Millions of buyers utilized this incentive, creating a short-term boost in transaction activity. Without awareness of such policy interventions, investors might mistakenly attribute rising demand to underlying market strength rather than temporary government support.

As real estate 2026 predictions take shape, staying informed about fiscal incentives, housing policy reforms, and regulatory adjustments will be essential for accurately interpreting market signals and avoiding mispriced assumptions.

Strategic Takeaway for Real Estate 2026 Predictions: Demographics, financing conditions, economic health, and government policy do not operate in isolation. Together, they form the structural foundation of real estate market behavior. In 2026, success will increasingly favor investors and operators who understand how these forces interact-and who position their portfolios ahead of demographic shifts, interest rate cycles, and policy-driven distortions.

4. Real Estate 2026 Predictions by Market Segment

Key takeaways for 2026 includes:

-

U.S. home values are projected to rise modestly by approximately 1.2% in 2026, while the number of major metros experiencing year-over-year price declines is expected to shrink significantly.

-

Existing-home sales are forecast to reach around 4.26 million transactions, reflecting a low single-digit increase as affordability gradually improves and sidelined buyers re-enter the market.

-

Rental affordability is set to improve further, with apartment rents expected to grow at a minimal pace, easing cost-of-living pressures for many households.

Overall, the housing market in 2026 is expected to move into a more stable phase. Buyers may benefit from reduced volatility and greater choice, while sellers could see steadier pricing supported by consistent-though not overheated-demand.

Residential Housing Market Outlook:

4.1. Home Prices: Modest Growth, Greater Stability

Following a largely flat performance in 2025, national home values are expected to edge higher by real estate 2026 predictions. This projected increase reflects slowly improving affordability, supported by incremental declines in financing costs and more balanced supply-demand conditions. Rather than rapid appreciation, most regions are likely to experience controlled, sustainable price growth.

4.2. Negative Equity Risks Ease

As prices stabilize across the majority of large metropolitan areas, fewer homeowners are expected to see their property values fall below purchase prices. This marks a shift from 2025, when price declines were still widespread across major markets. Improved price stability allows homeowners to preserve or gradually rebuild equity, reducing systemic risk in the housing market.

4.3. Mortgage Rates: Higher Than Pre-Pandemic Norms

While predicting interest rates remains inherently uncertain, mortgage rates in 2026 are widely expected to remain above the 6% threshold. Although these levels are far from the ultra-low rates of the pandemic era, gradual adjustments have already improved affordability compared to recent years. This environment is likely to encourage cautious re-entry from buyers who have adapted to the “new normal” of higher borrowing costs.

4.4. Transaction Activity: Slow Release of Pent-Up Demand

Existing-home sales are projected to rise modestly in 2026 as long-suppressed demand begins to resurface. Years of constrained inventory and elevated mortgage rates created a backlog of potential buyers. Early signs of renewed market activity suggest that continued improvements in affordability could support a stronger spring and fall selling season, provided economic conditions remain stable.

4.5. New Construction: A Challenging Year Ahead

The new-home construction sector is expected to face one of its weakest years since before the pandemic. Builders continue to manage elevated inventories and projects already in the pipeline, limiting the need for aggressive new starts. Single-family housing starts are projected to decline further, pushing annual totals below recent lows.

To maintain buyer interest, developers are likely to rely heavily on incentives such as rate buy-downs and pricing concessions, particularly in markets where affordability remains strained. As a result, new construction will remain selective rather than expansive in 2026.

5. Real Estate 2026 Predictions: Rental Market Outlook

Rental market outlook for 2026 predictions.

5.1. Renters See Improved Affordability

Rental conditions are expected to remain favorable for tenants across much of the country. With income growth continuing to outpace rent increases in many large metros, the share of household income spent on rent has declined to its lowest level in several years. Apartment rents are forecast to grow only marginally in 2026, giving renters additional financial breathing room.

Single-family rental rates, however, may rise more noticeably as would-be buyers postpone homeownership and remain in the rental market longer.

5.2. Regional Exceptions

Not all markets will follow the national trend. In cities such as New York, rental growth is expected to accelerate, driven by persistent demand, limited supply, and lifestyle-driven migration patterns.

5.3. Lifestyle Renters Gain Influence

Renting is increasingly a long-term lifestyle choice rather than a transitional phase. A growing share of renters prioritize flexibility, reduced maintenance responsibilities, and alignment with personal or professional mobility. Surveys indicate that a majority of renters plan to continue renting into 2026, even if mortgage rates decline.

5.4. “Kidfluence” Shapes Rental Demand

Household composition is also reshaping rental preferences. A rising percentage of renters now live with children, influencing demand for family-friendly amenities and layouts. Properties offering features such as learning spaces, creative play areas, and flexible communal zones are expected to outperform as family-oriented renters become a more influential segment.

In markets like New York City, shared living spaces and thoughtfully designed common areas are forecast to become defining characteristics of competitive rental developments.

5.5. Inflation-Resilient Home Features Gain Popularity

Persistent cost-of-living pressures are redefining what buyers and renters value in a home. Energy-efficient and cost-saving features-such as solar integration, home battery systems, EV charging, and optimized storage-are appearing more frequently in listings. Homes designed to support bulk purchasing, food preservation, and efficient energy use are expected to gain traction as households seek greater financial resilience.

5.6. AI Evolves into a Transaction Coordinator

By 2026, artificial intelligence is expected to move beyond basic recommendations and into an orchestration role within real estate transactions. AI systems will increasingly manage end-to-end processes-matching buyers and sellers with suitable agents, scheduling viewings, supporting negotiations, and coordinating closing steps. This “agentic AI” approach has the potential to reduce friction, automate routine tasks, and make outcomes more predictable for all parties involved.

Taken together, real estate 2026 predictions point to a market defined less by dramatic swings and more by structural adjustment. Stability, segmentation, and technology-driven efficiency will be key themes. Participants who align their strategies with evolving affordability dynamics, renter behavior, and AI-enabled workflows will be best positioned to succeed in the next phase of the real estate cycle.

6. Visual Marketing Becomes a Competitive Differentiator

As the U.S. housing market moves into a more balanced and selective phase in 2026, competition among listings is increasingly shifting from price alone to presentation quality. Longer days on market and more negotiating leverage for buyers mean that properties must work harder to capture attention across digital platforms. High-quality photography, video walkthroughs, and visual consistency are becoming essential-not optional-tools for standing out in crowded marketplaces.

In this environment, many real estate professionals are reassessing how they scale visual production efficiently without sacrificing quality or turnaround time. Hybrid workflows that combine AI-assisted enhancements with professional human editing are gaining traction, allowing agents, photographers, and brokerages to maintain marketing standards while managing cost and volume. Service providers such as Fotober support this transition by helping real estate teams optimize visual assets at scale, aligning marketing execution with the evolving demands highlighted in real estate 2026 predictions.

7. Conclusion: What Real Estate 2026 Means for the Industry

As the U.S. real estate market moves into 2026, the narrative is no longer defined by rapid rebounds or sharp corrections, but by structural adjustment and selective growth. The volatility of the post-pandemic years has given way to a more disciplined environment where affordability, financing conditions, and asset quality dictate outcomes more than speculation or short-term momentum.

Across residential and rental segments, demand remains intact but increasingly segmented. Buyers and renters alike are recalibrating expectations-prioritizing efficiency, value, and long-term cost resilience over size or location alone. At the same time, elevated interest rates and tighter credit conditions continue to filter out weaker projects, reinforcing a market that rewards realistic pricing, thoughtful design, and operational efficiency.

Technology will play a decisive role in this next phase. From AI-driven transaction coordination to data-informed investment decisions, real estate in 2026 is becoming less about volume and more about precision. Properties that are well-positioned, well-presented, and aligned with evolving consumer preferences will stand out in a market where competition is quieter but more strategic.

Ultimately, real estate 2026 predictions point toward a market that is neither booming nor collapsing-but maturing. For investors, developers, and service providers, success will depend on adaptability, clarity of strategy, and the ability to respond to nuanced shifts rather than broad cycles. Those who understand the underlying forces shaping demand-and position themselves ahead of them-will be best equipped to navigate the next chapter of the U.S. real estate market.

---------------------------------------------

Fotober is a professional real estate photo editing company trusted by photographers and real estate professionals to enhance property images with precision, speed, and consistency.

- Facebook: fotobermedia.co

- Youtube Channel: Fotober

- TikTok Channel: @fotober

- Instagram: fotobervn

- Email supporter: [email protected]

- Hotline: +84 942 110 297

Related posts

Winning Buyers With These Las Vegas Real Estate Photography Top Picks

July 29, 2026

Luxury Real Estate Marketing Trends California Agents Love in 2026

July 27, 2026

Reno Real Estate Photography: Top Studios for Selling Homes Faster

July 27, 2026

Las Vegas Virtual Staging: Best Platforms to Enchant Your Listings

July 23, 2026